Ten Key Global Risks for Businesses

The Dun & Bradstreet Global Business Risk Report (GBRR) ranks the biggest threats to business based on each risk scenario’s potential impact on companies, assigning a score to each risk. The scores from the top ten risks are used to calculate an overall Global Business Impact (GBI) score.

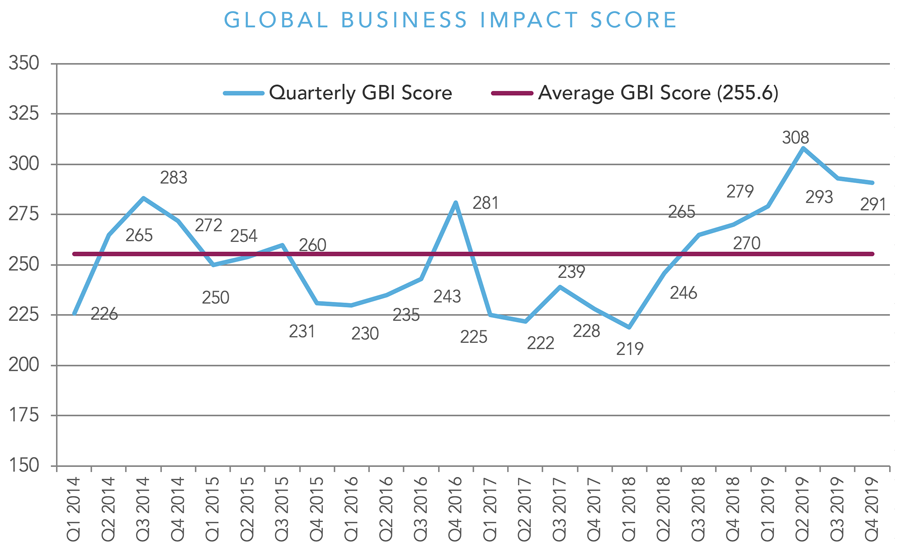

Our latest GBI score highlights a second successive slight quarterly improvement in outlook for cross-border businesses, after the score hit its worst-ever level in Q2.

Risks still extreme

Dun & Bradstreet’s GBI score has improved marginally for a second successive quarter, having reached a record high of 308 in Q2 2019. However, the Q4 score of 291, although better, is still at an elevated level, indicating that the global business operating environment remains fraught. The Q4 score is the third-highest since the measure was launched in 2013, and is well above the long-term average (255.6). Despite the improvement this quarter, the current score shows that there has been a significant worsening in business risk since Q1 2018 – when the best-ever score of 219 was recorded.

Our top ten risks combine an assessment of: (i) the magnitude of the event’s probable effect on the global business operating environment, on a scale of 1 to 5 (where 1 is the smallest impact and 5 is the largest); and (ii) the likelihood of the event happening.

Seven new risks in the global top ten

Highlighting the ever-evolving global environment, there are a record seven new entries in our Q4 2019 GBRR’s top ten: two from Western & Central Europe, two pan-regional ones, and one each from North America, Asia-Pacific, and Eastern Europe & Central Asia.

The seven new-entry risks are:

- The ECB injects more monetary stimulus, thereby keeping the value of the euro low: this could lead to the implementation of US trade barriers, curtailing global trade and hence business opportunities (GBI of 36, out of a maximum 100);

- The impeachment inquiry moves the US towards greater division and undermines the bipartisan political dynamic, making a government shutdown in late November highly likely and rocking global financial markets (GBI of 30);

- Global tech sector valuations and investment collapse in the context of unexpected national security barriers to supply chains, trade and investment, as markets factor in country-specific risks. Venture capital and commercial real estate markets in prime business centres go into shock (GBI of 27);

- Technological threats, predominantly driven by artificial intelligence, lead to economic damage and geopolitical risks. Threats of cyber-attacks, data theft, fraudulent activities by state and non-state actors, and the risks of outages of information and networks rise continuously (GBI of 27);

- Russia uses Western Europe’s over-reliance on its energy exports to promote a more assertive regional policy, disrupting business relations between Russia and Europe (GBI of 27);

- The decline of centre-right and especially centre-left mainstream parties continues, leading to more EU-sceptic governments in Europe, complicating policy-making in the EU and undermining the business environment (GBI of 27); and

- In China, contagion from bad debts in industry and local government triggers a financial crisis in smaller banks and emergency recapitalisations, which lay bare the weaknesses in a string of struggling provincial economies (GBI of 26).

Among the pre-existing risks in our top ten, two GBI scores improved, while one stayed the same. The Q4 top ten highlights the geographical diversity of risks facing businesses in today’s environment, with three risks emanating from Western & Central Europe, two from North America, one from Asia-Pacific, and one from Eastern Europe & Central Asia; three pan-regional risks complete the top ten. The types of risk also remain diverse, and are associated with policy-making (3), politics (3), structural issues (2) and economic developments (2). This reinforces the fact that finance, procurement and supply-chain teams across all business sectors need to combat the impacts of an increasingly complex and globalised world.

Policy-making failures could undermine trade flows

The top two risks in the latest GBRR are associated with policy-makers and how their decisions could undermine global trade flows. In equal first place, with a GBI of 36 (down from 42 in the previous report) is our concern that policy-makers will be unable to negotiate a settlement that will stop the US-China trade war. This failure would lead to a spiralling of the conflict, with negative secondary effects offsetting new business opportunities and undermining global trade volumes.

Also in equal first place – and the highest new entry, with a GBI of 36 – is our concern that policy-makers in the US respond negatively to further monetary stimulus by the ECB (which would keep the value of the euro lower). In response, the US could increase trade barriers to EU exports, curtailing trade flows and thus undermining business opportunities.

The final policy-making risk factor is that decision-makers erect national security barriers to supply chains, trade and investment, as markets factor in country-specific risks. This would impact negatively on global tech sector valuations and investment flows, with a particular emphasis on venture capital and commercial real estate markets in prime business centres. This pan-regional factor has a GBI of 27 and is in equal fifth place.

Political concerns

Each of the three political concerns is a new entry. Our first political concern, with a GBI of 30, and in third place overall, is that the potential fall-out from the ongoing US presidential impeachment inquiry leads to greater bipartisan polarisation, resulting in a high likelihood (75%) of a government shutdown occurring in late November, rocking global financial markets.

The second political concern is in equal fifth place with a GBI of 27. Our worry is that Russia uses Western Europe’s over-reliance on Russian energy exports to promote a more assertive regional policy, disrupting relations between Russia and Europe – making doing business more difficult. Also in equal fifth place with a GBI of 27 is the final political issue, which emanates from Western & Central Europe. We are concerned that the decline of centrist mainstream parties in Europe will continue, leading to more EU-sceptic governments, thereby complicating policy-making in the EU and undermining the business environment.

Structural impediments

Two longer-term structural issues feature in our top ten risks. In fourth place, with a GBI of 28 (the same as the previous report), is that labour scarcity and anti-immigration policies in Western & Central Europe lead to a fall in long-term EU growth potential, undermining global business opportunities. The second structural risk is of economic damage and geo-political harm stemming from technological threats, predominantly driven by artificial intelligence. Threats of cyber-attacks, data theft, fraudulent activities by state and non-state actors, and the risks of outages of information and networks are rising continuously. This pan-regional factor is a new entry and is in equal fifth place with a GBI of 27.

Economic concerns

Two economic risks take up the remaining places in our top ten. In equal fifth place with a GBI of 27, down from 39 (and second place) in our previous report, is our concern that the current expansion in the US has reached its peak, leading to a turning point in the credit cycle and eventually the US business cycle, in turn impacting global prospects.

The second economic impact is a new entry in tenth place and has a GBI of 26. Here, we are concerned that contagion from bad debts in industry and local government in China triggers a financial crisis in smaller banks, with the need for emergency recapitalisations. This would lay bare the weaknesses in a string of struggling provincial economies.

Summary: Business environment risk eases slightly

Dun & Bradstreet’s Global Business Impact score for Q4 2019 shows that the risks confronting businesses remain elevated by historical standards, despite a marginal improvement compared with the previous quarter (down to 291, from 293). The Q4 2019 score highlights that business decision-makers still need to monitor the global business environment continually and carefully as the global economy slows once again. The geographical spread and diversity of risks related to policy-making, politics, longer-term structural issues and economic developments make the business environment increasingly challenging.

Top ten risks

| Ranking | Region | Risk | Likelihood of Event (%) | Global Impact (1-5) | Global Business Impact Score (1-100) |

|---|---|---|---|---|---|

| =1 | Pan-regional | Negotiations fail to stop a US-China trade war, which spirals, with negative secondary effects offsetting new opportunities and cooling global trade growth. | 60 | 3 | 36 |

| =1 | Western and Central Europe | The ECB injects more monetary stimulus, thereby keeping the value of the euro low; this could lead to the implementation of US trade barriers, curtailing global trade and hence business opportunities. | 60 | 3 | 36 |

| 3 | North America | The impeachment inquiry moves the US toward greater division, and bipartisan co-operation collapses, making a government shutdown in late November highly likely and rocking global financial markets. | 75 | 2 | 30 |

| 4 | Western and Central Europe | Labour scarcity and anti-immigration policies lead to a drop in long-term EU growth potential, undermining global business opportunities. | 70 | 2 | 28 |

| =5 | Pan-regional | Global tech sector valuations and investment collapse in the context of unexpected national security barriers to supply chains, trade and investment, as country risk factors return. Venture capital and commercial real estate markets in prime business centres go into shock. | 45 | 3 | 27 |

| =5 | Pan-regional | Technological threats, predominantly driven by artificial intelligence, lead to economic damage and geopolitical risks. Threats of cyber-attacks, data theft, fraudulent activities by state and non-state actors, and the risks of outages of information and networks rise continuously. | 45 | 3 | 27 |

| =5 | Eastern Europe and Central Asia | Russia uses Western Europe's over-reliance on its energy exports to promote a more assertive regional policy, disrupting business relations between Russia and Europe. | 45 | 3 | 27 |

| =5 | North America | Peak rates in the US have been reached for the current expansion, leading to a turn in the credit cycle and eventually the US business cycle; in turn, impacting global prospects. | 45 | 3 | 27 |

| =5 | Western and Central Europe | The decline of centre-right and especially centre-left mainstream parties continues, leading to more EU-sceptic governments in Europe, complicating policy-making in the EU and undermining the business environment. | 45 | 3 | 27 |

| 10 | Asia-Pacific | In China, contagion from bad debts in industry and local government triggers a financial crisis in smaller banks and emergency recapitalisations, which lay bare the weaknesses in a string of struggling provincial economies. | 65 | 2 | 26 |