The insurance sector has been relatively slow to adopt the digital, data-centric future, but it's steadily becoming a primary focus due to improved effectiveness and enhanced customer education understanding.

The report, Digital Modernization in the Insurance Industry: How to Drive Progress in Your Organization, produced by EPAM Systems and backed by London Research, reveals a key finding: insurance companies acknowledge the necessity of change. Less than half of the companies surveyed categorize themselves as 'advanced' in the main areas of business evolution. Only slightly more consider their progress ‘significant.'

Business transformation has been an uninviting prospect in the insurance industry for some time. One respondent explained, “When the business model is operational, convincing stakeholders you need to modify something can be taxing. They argue that we already generate gigantic profits, so why do we need to change our operations?”

Yet, various coexisting trends are now shaking up the sector, common across all verticals, including some relating explicitly to insurance. Here are a few catalysts of change:

The Ghost of Outdated Technology

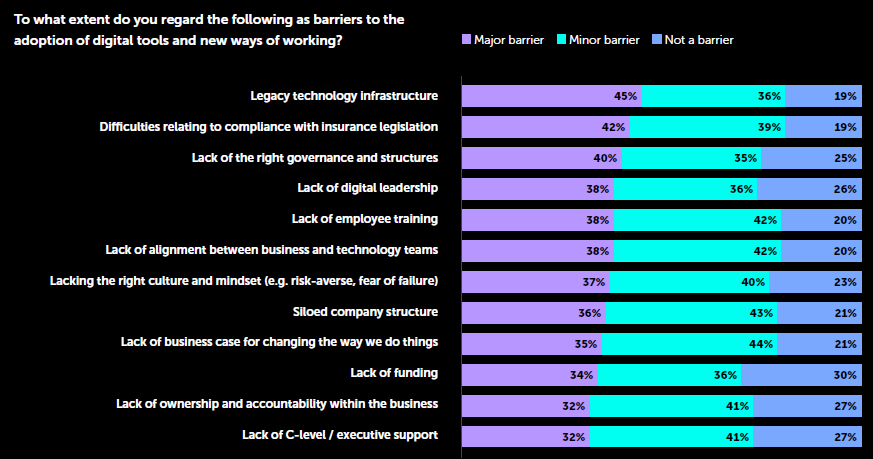

Legacy technology infrastructure is the most significant obstacle for insurance companies aspiring to harness digital tools and adopt unique operational methods. In fact, it's a major barrier for 45% of surveyed companies. It inhibits innovation, compromises client experience and slows down speed-to-market. Legacy technology burdens IT teams with maintaining and upgrading it, while makeshift solutions implemented by disgruntled employees are setting up future problems for the IT department.

There are other factors amplifying this outdated tech issue: a lack of digital leadership (identified as a significant issue by 38%), misalignment between business and IT (38%), absence of a business case for change (35%), lack of funding (34%) and insufficient executive backing (32%).

Natasha Davydova, CIO at AXA says — “An example of legacy technology slowing down the transformation of business might be where it’s supporting very old products, and your new systems don’t cater to those products any longer. Very often businesses are reluctant to move away from those legacy systems because they’re supporting a particular book of clients, usually in annuities. Some technologies have been running books of business for many, many years, so businesses can end up running new and old systems in parallel.”

Are Insurers Prepared to Adopt AI?

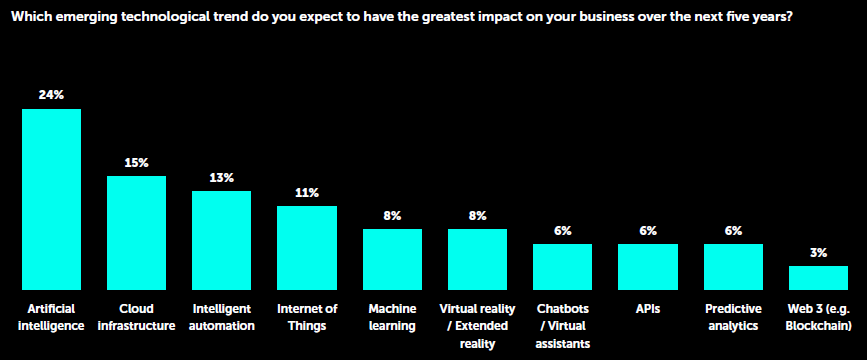

Nearly three in five companies (57%) remarked that recent developments in Artificial Intelligence (AI) and machine learning are making a notable impact on their business, with 24% anticipating it will be the most influential in the next five years. A third also claimed this as the tech that will cause the most substantial business shift in the next five years, topping the list of choices.

AI has several benefits; therefore, it's not surprising that executives lean towards it. With numerous use cases to consider, AI is applicable across all insurance sectors, departments and entire value chains. However, these newer capabilities can only start their journey with the right access to the business’s data and the necessary supporting infrastructure.

Executives Understand the Value of Technology Enablement, but Investment Is Slow to Follow

The survey paints a picture of an industry that, at an executive level, understands the necessity for a more advanced embrace of technology, but hasn't properly aligned the investment needed to do so. This suggests that the prospective value technology could bring to the business isn't being fully harnessed, leading to further constraints on tech funding. Revamping legacy systems is often immensely disruptive for an organization, and insurers frequently lack a dire necessity for such drastic reforms. Culturally, they've also struggled with embracing the "Fail Fast" or "Learn and Adapt" mindset, as most executive sponsors have failed to witness the benefits and tend to interpret it as sheer failure.

When being interviewed for the research, a senior executive said, “Most insurance companies are 50 to 100+ years old, and they’re operating on a very mature business model. That has implications for digital transformation because as long as the business model works, it’s quite challenging to convince the stakeholders that we need to change because they’ll tell you that we make good profits, so why do we need to change the way? As long as the business model works, it’s quite challenging to convince the stakeholders that we need to change because they’ll tell you that we make good profits, so why do we need to change how we operate? And there’s no pressure from disruptors or insuretechs to change the model either.”

Moving Ahead

As the insurance industry embarks on a new era, these outcomes underscore an urgent need for digital modernization. Even though the journey is complex and multifaceted, the path forward is clear: encouraging innovation, prioritizing customers and establishing a robust, future-centric technology infrastructure. Leaders need to take decisive action in three key areas:

1. Invest Strategically in Emerging Technologies: Prioritize allocating resources towards technologies that not only streamline operations but also unlock new avenues for market engagement and product innovation.

2. Cultivate an Agile Organizational Mindset: Encourage a culture of innovation that embraces change, values cross-functional collaboration and empowers employees to think creatively about solving industry challenges.

3. Leverage Data to Drive Decision-Making: Harness the vast amounts of data at your disposal to inform strategic decisions, personalize customer experiences and anticipate market trends.

For a deep dive into the topics discussed in this article, read the Digital Modernization in the Insurance Industry: How to Drive Progress in Your Organization Report, produced by London Research in collaboration with EPAM Systems, available for download here.